|

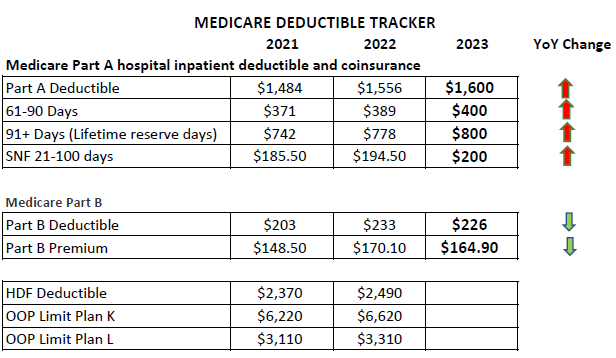

Medicare Part B Premium and Deductible Medicare Part B covers physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A. Each year the Medicare Part B premium, deductible, and coinsurance rates are determined according to the Social Security Act.

The 2022 premium included a contingency margin to cover projected Part B spending for a new drug, Aduhelm. Lower-than-projected spending on both Aduhelm and other Part B items and services resulted in much larger reserves in the Part B account of the Supplementary Medical Insurance (SMI) Trust Fund, which can be used to limit future Part B premium increases. The decrease in the 2023 Part B premium aligns with the CMS recommendation in a May 2022 report that excess SMI reserves be passed along to people with Medicare Part B coverage. Beginning in 2023, certain Medicare enrollees who are 36 months post kidney transplant, and therefore are no longer eligible for full Medicare coverage, can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. For 2023, the immunosuppressive drug premium is $97.10. Medicare Open Enrollment and Medicare Savings Programs Medicare Open Enrollment for 2023 will begin on October 15, 2022 and ends on December 7, 2022. During this time, people eligible for Medicare can compare 2023 coverage options between Original Medicare, and Medicare Advantage, and Part D prescription drug plans. In addition to the soon-to-be released premiums and cost sharing information for 2023 Medicare Advantage and Part D plans, the Fee-for-Service Medicare premiums and cost sharing information released today will enable people with Medicare to understand their Medicare coverage options for the year ahead. Medicare health and drug plan costs and covered benefits can change from year to year, so people with Medicare should look at their coverage choices annually and decide on the options that best meet their health needs. To help with their Medicare costs, low-income seniors and adults with disabilities may qualify to receive financial assistance from the Medicare Savings Programs (MSPs). The MSPs help millions of Americans access high-quality health care at a reduced cost, yet only about half of eligible people are enrolled. The MSPs help pay Medicare premiums and may also pay Medicare deductibles, coinsurance, and copayments for those who meet the conditions of eligibility. Enrolling in an MSP offers relief from these Medicare costs, allowing people to spend that money on other vital needs, including food, housing, or transportation. People with Medicare interested in learning more can visit: https://www.medicare.gov/your-medicare-costs/get-help-paying-costs/medicare-savings-programs. Medicare Part B Income-Related Monthly Adjustment Amounts Since 2007, a beneficiary’s Part B monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 7 percent of people with Medicare Part B. Medicare Part A Premium and Deductible Medicare Part A covers inpatient hospital, skilled nursing facility, hospice, inpatient rehabilitation, and some home health care services. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment. The Medicare Part A inpatient hospital deductible that beneficiaries pay if admitted to the hospital will be $1,600 in 2023, an increase of $44 from $1,556 in 2022. The Part A inpatient hospital deductible covers beneficiaries’ share of costs for the first 60 days of Medicare-covered inpatient hospital care in a benefit period. In 2023, beneficiaries must pay a coinsurance amount of $400 per day for the 61st through 90th day of a hospitalization ($389 in 2022) in a benefit period and $800 per day for lifetime reserve days ($778 in 2022). For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $200.00 in 2023 ($194.50 in 2022).

|

PSM was a proud sponsor of this years AAHU Golf Tournament held at Balcones Woods country club in Austin.

It was a wonderful event and a great opportunity to network with other insurance professionals and discuss the changes shaping our industry. We appreciate all those who attended and contributed and can't wait for next years event!

|

About AAHU AAHU - The Austin Association of Health Underwriters is a local chapter of the National Association of Health Underwriters,(NAHU) and the Texas Association of Health Underwriters (TAHU) a volunteer member organization that represents nearly 20,000 licensed health insurance agents, brokers, consultants, and benefit professionals through more than 200 chapters across America. AAHU members help Central Texas consumers by guiding them through the complexities of Health, Dental, Disability, Medicare Supplements and Life insurance benefit decisions for businesses and individuals. Our organization is dedicated to providing professional development opportunities to our members so they can better serve their clients insurance needs.

The SIMS Foundation provides mental health and substance use recovery services and supports for musicians, music industry professionals, and their dependent family members. Through education, community partnerships, and accessible managed care, SIMS seeks to destigmatize and reduce mental health and substance use issues, while supporting and enhancing the wellbeing of the music community at large.

|